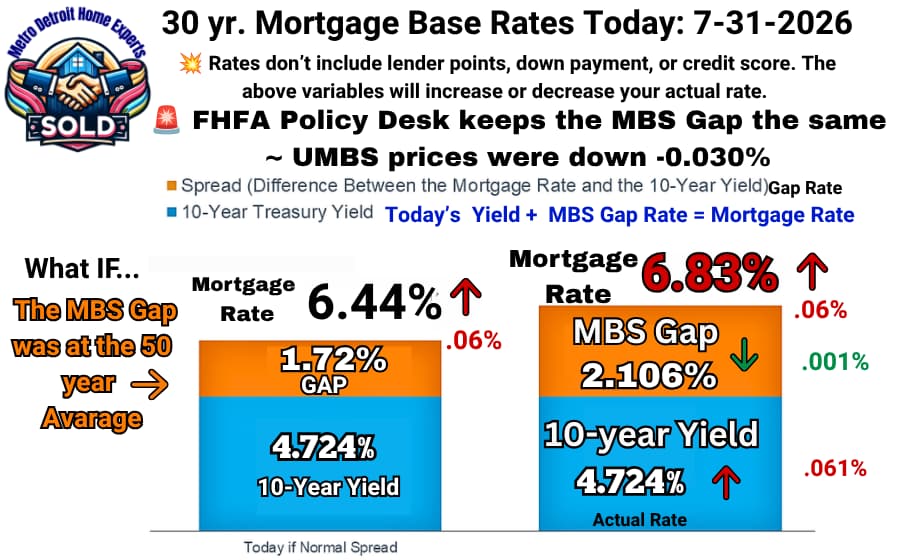

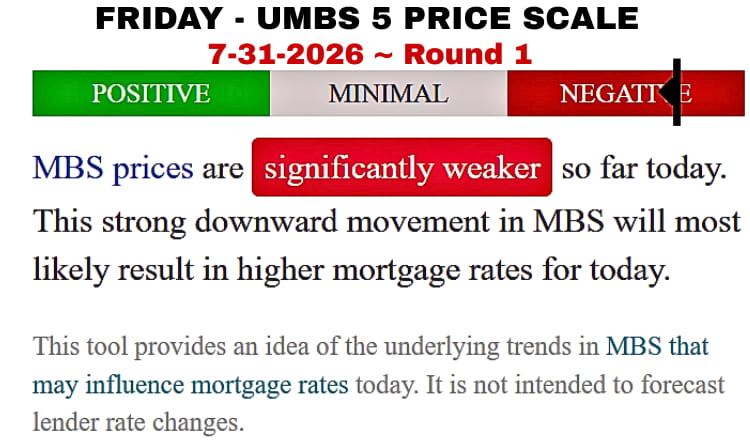

📌 Today’s MBS Gap: Hero 🦸 or Villain 🦹Mortgage Rate Lock Alert for 7-31-2026 🕚 11:00 UMBS Prices

💡 Remember the bond market is live and drifts constantly. That’s why we watch the market up to 1:00 for repricing. The FHFA Policy Desk and the GSEs (Freddie Mac and Fannie Mae) select the time to anchor ⚓the yield and the MBS gap based on UMBS 5 pricing.

🦸 hERO Scenario: Today’s Math IF FHFA Policy Desk Compressed the Gap: The FHFA policy desk artificially compressed the gap yesterday; I can’t imagine they’ll do it again today. The yield at 10:00 ⚓ at 4.731%, plus the MBS gap range of 2.097% to 2.087% (-0.010 to -0.020) will land mortgage rates at 6.82% to 6.81%. The yield at 10:30 ⚓ at 4.724%, plus the MBS gap range of 2.097% to 2.087% (-0.010 to -0.020) will land mortgage rates at 6.82% to 6.81%. ⚠️Possible repricing 📈📉 in the afternoon if there is a drift. ⚓

⚖️ Balanced Scenario: Today’s Math Applied: The 10:00 yield at 4.731%, plus Yesterday’s MBS gap artificial compression of 2.107%, puts mortgage rates at 6.84%. The 10:30 yield at 4.724%, plus Yesterday’s MBS gap of 2.107%, puts mortgage rates at 6.83%. ⚠️Possible repricing 📈📉 in the afternoon if there is a drift. ⚓

🦹 Villain Scenario: Today’s Gap Correction IF Applied: The yield at 10:00 ⚓ at 4.731%, plus the MBS gap range of 2.117% to 2.137% (+0.010 to +0.030) will land mortgage rates at 6.85% to 6.87%. The yield at 10:00 ⚓ is 4.724%, plus the MBS gap range of 2.117% to 2.137% (+0.010 to +0.030) will land mortgage rates at 6.84% to 6.86%.⚠️Possible repricing 📈📉 in the afternoon if there is a drift. ⚓