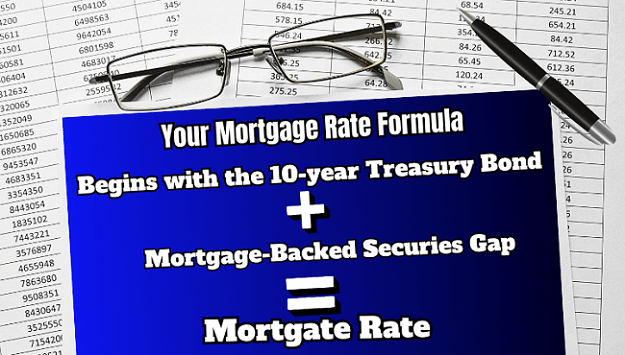

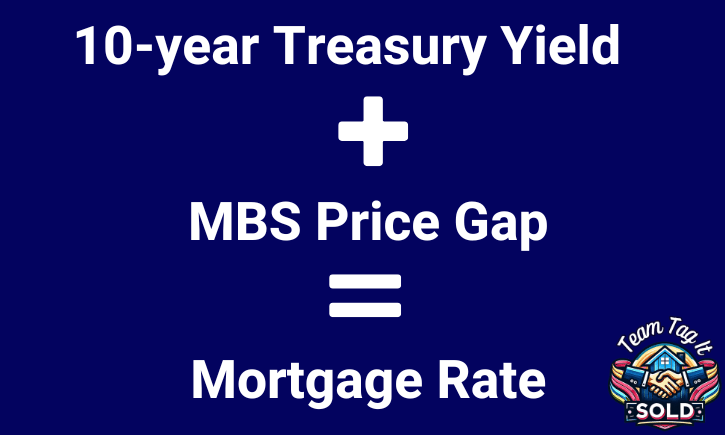

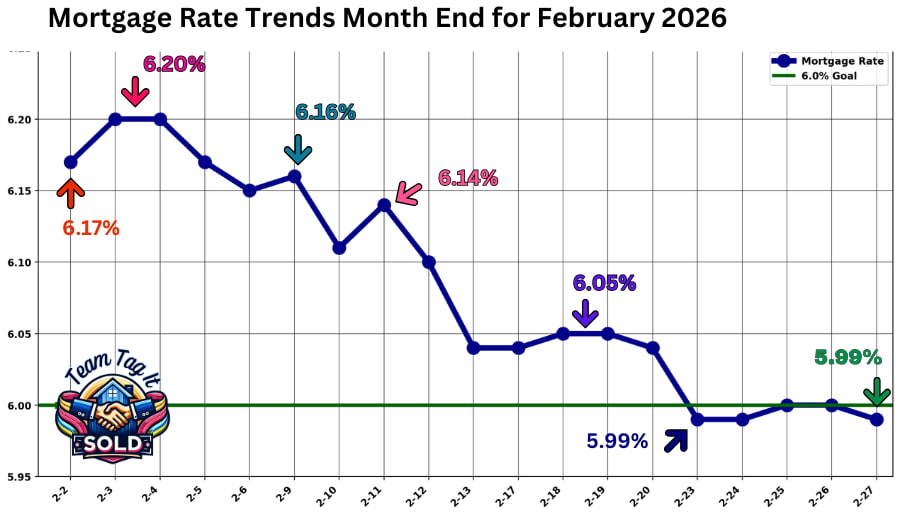

Step 1: Why the Yield is Dipping 📉

It appears the mechanics and math will influence mortgage rates moving forward. Wall Street is closely monitoring the policies and the Treasury bond market. The Treasury auction has been extremely weak for months, and investors are jumping in ONLY IF the Treasury is covering their risk and offering higher coupon rates. Those higher coupon rates are what are causing the yield to spike. It’s going to take months before we feel relief from inflation, because the goods on shelves and in warehouses were purchased under the higher tariff regime.

1️⃣ Bond market reaction to Tariff Policies 📉

The Fed’s latest messaging reinforced that rate cuts are not guaranteed yet. Officials want more confirmation that inflation is sustainably cooling before shifting policy. Even without raising rates, this “wait for proof” stance keeps upward pressure on yields and mortgage pricing because markets must price in the risk that policy stays restrictive longer.

3️⃣ Labor market signals remain mixed 💼

While longer-term trends show cooling hiring and rising continuing claims, the most recent weekly data did not confirm a rapid deterioration in labor conditions. When jobless claims fail to show meaningful acceleration, investors assume the economy remains stable, reducing the urgency for lower rates and nudging yields higher. The issue here is that initial jobless claims and unemployment are based on a survey, not on actual numbers from each state’s unemployment rolls. In this day and age, I don’t understand why we don’t have actual numbers for accurate measurements, so much for transparency.

4️⃣ Consumer spending is slowing but not collapsing, YET 🛍️

Retail sales have weakened compared to earlier momentum, reinforcing the narrative of a cooling consumer, yet the slowdown is gradual rather than recessionary. Markets typically need clear deterioration — not moderation — to push mortgage rates meaningfully lower. December year-over-year retail was down 2.3% from 4.7% to 2.4%

5️⃣ Payroll data credibility and market skepticism 📊

Markets continue to weigh the differences among ADP payroll data, jobless claims trends, and BLS reporting. That uncertainty creates volatility. When investors lack conviction that the economy is weakening quickly, bond markets hesitate to rally, which prevents mortgage rates from sustaining downward momentum.

✅ Bottom line:

Mortgage rates moved slightly higher yesterday after bond yields rose, even as the Fed’s caution and labor data failed to confirm rapid economic weakness. The broader trend still reflects a slowing economy, but until investors see clearer signs of deterioration — especially in jobs and inflation —ate increases will likely remain uneven and temporary.

More Help Is ONE Click Away⤵️

Pick Your Topic by Scrolling

Today’s Mortgage Rates: What’s Driving the Change 📈📉

Home Pricing Missteps 😱

Negotiation Strategies for Home Buyers and Sellers 🙌🏡

New Construction in Metro Detroit: Homes for Sale W/Video🏡🔎

Home Purchasing Power – Do You Know Your’s❓🏡

FHA Mortgage: What is It and How Can You Benefit in Metro Detroit

Real Estate Guides for Buying and Selling a Home📚

Discover How Home Equity Can Fund Your Next Move💰

Top 3 Home Selling Questions Answered 🏡❓

Metro Detroit MI Housing Market Trends by City 🔎📊

Metro Detroit MI Homes for Sale by City 🏘️🎯

Metro Detroit MI Sold Home Prices by City

Learn How To Master Pricing Your Home Like a Pro 💥🏡

1st-Time Homebuyers: Tips to Make Your Dream Come True🏡🥳

1st-Time Homebuyers Saving Strategies🏡🔑💲

Is Owning a Home Still Your Dream – Help is Here💥🏡

Home Down Payment Assistance Programs : Need Help? 🥰💯

Adjustable Rate Mortgage (ARM): Smart Move or Mistake❓

Home Value vs Price in Metro Detroit: Myth Busting Revealed 🤫

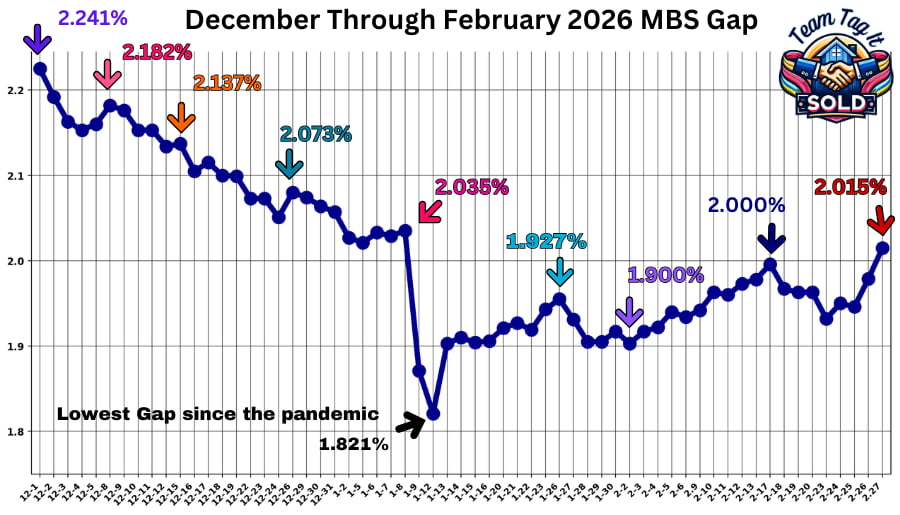

Mortgage-backed Securities Effects on Mortgage Rates💲📉

Your Home Equity Gains: Game Changer When You Sell🏠📈

Mortgage Pre-Approval: The Secret Power Buyers Need to Know 🎓💲

Buying a Fixer-Upper: Hidden Benefits Most Buyers Overlook 👀

Is it Still a Sellers Market Today in Metro Detroit🏡❓

Will Foreclosures Crash the Housing Market in Metro Detroit Winter 2025

How to Choose the Right Buyers Agent: A Must for Home Buyers’ 🛒

What Is A True Real Estate Expert: How to Find One🏡💥

Selling Your House As-Is OR Make Repairs Pros🌟 and Cons🚫

Top Real Estate Agent Skills for Selling Your Home🏡💲