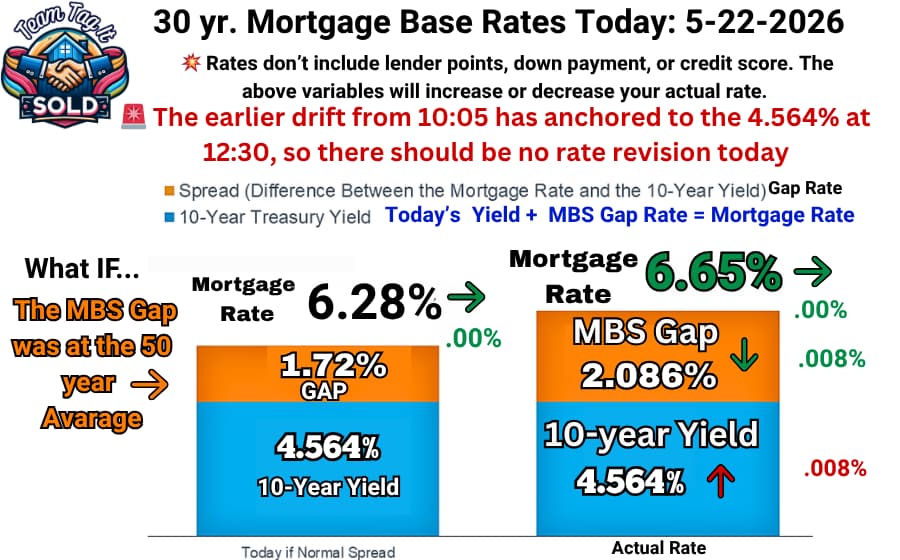

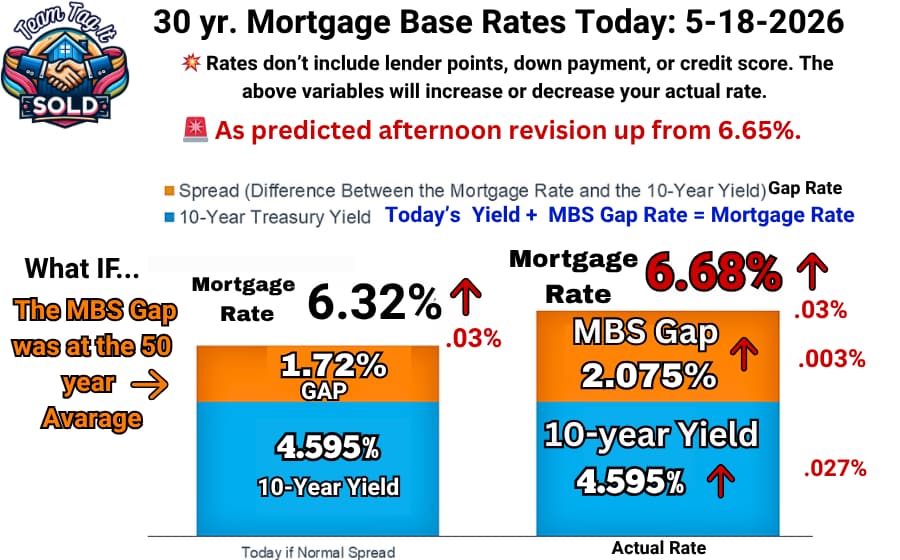

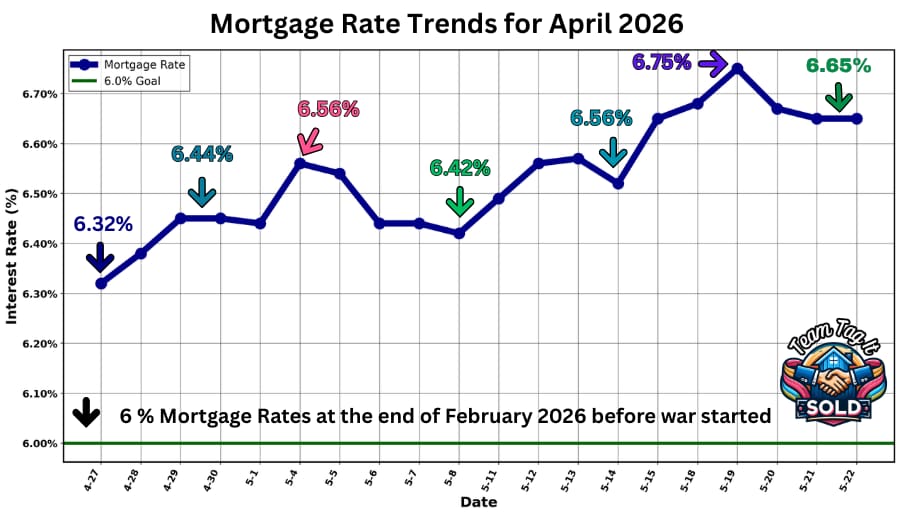

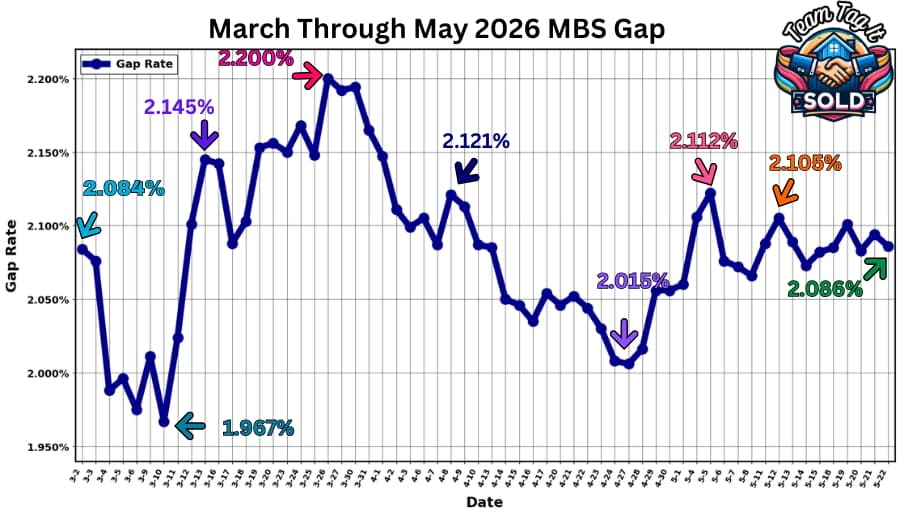

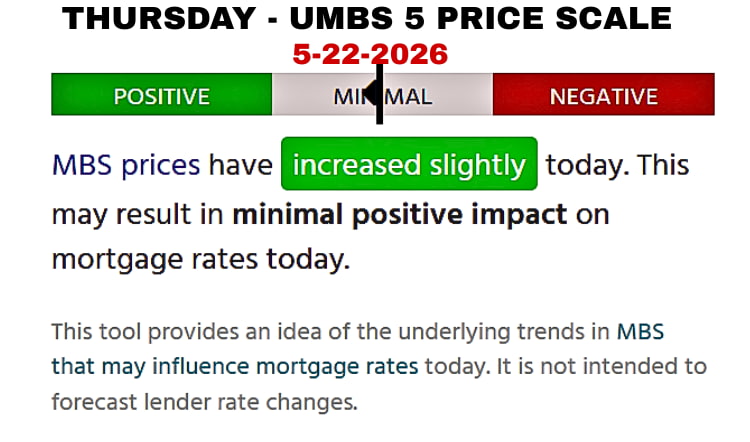

📌 Today’s MBS Gap: Hero 🦸 or Villain 🦹Prediction Range 5-22-2026 Today’s Range is 6.64% – 6.66%

💡 The FHFA Policy Desk and the GSEs (Freddie Mac and Fannie Mae) select the time to anchor ⚓the yield and the MBS gap based on UMBS 5 pricing. Today, there was a slight drift up at 10:30 to 4.572%.

🦸 Hero Scenario: Today’s Math IF Applied: The UMBS5 pricing increased slightly over yesterday. The 10:00 yield was 4.564%, plus -0.008 to -0.018 ( 2.086 to 2.076%), putting mortgage rates at 6.65% to 6.64%.

⚖️ Balanced Scenario: Today’s Math Applied: The 10:00 yield was 4.564%, plus yesterday’s MBS gap at 2.094%, putting mortgage rates at 6.66%. The 10:30 yield was 4.572%, plus yesterday’s MBS gap of 2.094%, bringing mortgage rates to 6.67%.

🦹 Villain Scenario: Today’s Math IF Applied: I don’t see a villain scenario today unless the FHFA policy desk and GSEs decide to close the MBS gap to offset prior gap compression. This would require a mind reader. 😂