More Help Is 1️⃣ Click Away⤵️

Pick Your Topic by Scrolling

Adjustable Rate Mortgage (ARM): Smart Move or Mistake❓

By Pam Sawyer 🤓

/ 10/25/2025

Thinking about an 🔁 Adjustable Rate Mortgage (ARM) in today’s market? Discover how ARMs work, what’s changed since the 2008 crash,…

Read More

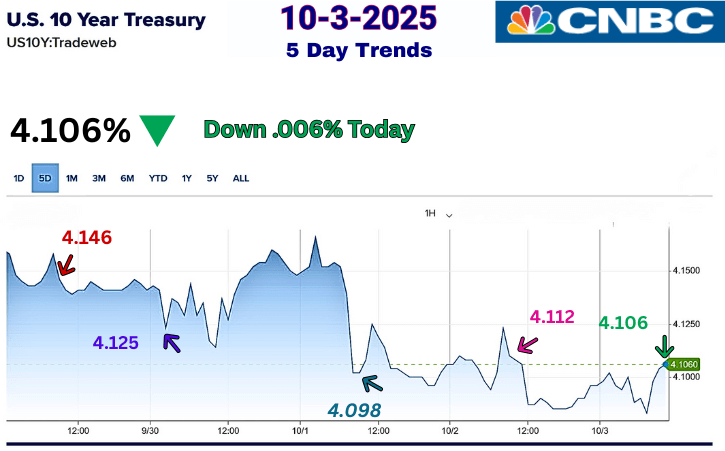

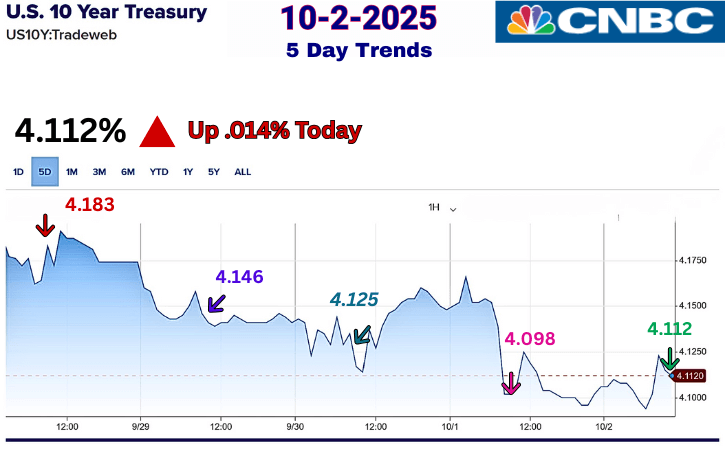

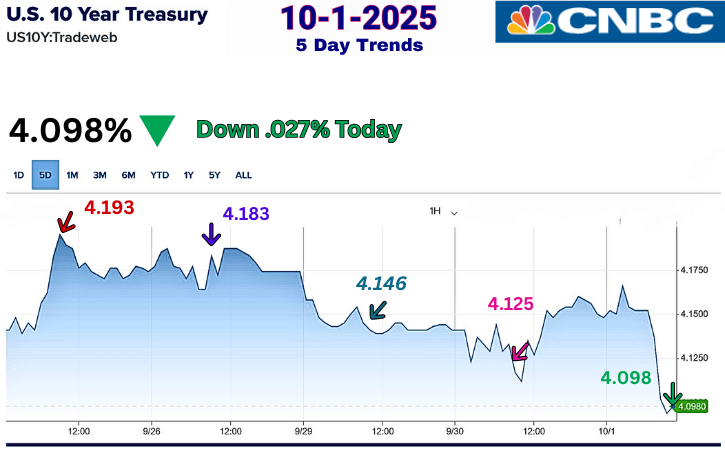

Today’s Mortgage Rate: Your Why Alert with Video 📢

By Pam Sawyer 🤓

/ 10/24/2025

Today’s Mortgage Rates: Let’s crack the code 🔢 for Metro Detroit and take control of your home financing! The video will help…

Read More

Metro Detroit Home Prices and Real Estate Trends by City~Oct.📊

By Pam Sawyer 🤓

/ 10/23/2025

🎯 Want the latest scoop on Metro Detroit home prices? 📊🏡 Our live MLS data and interactive charts keep you…

Read More

Home Value vs Price in Metro Detroit: Myth Busting Revealed 🤫

By Pam Sawyer 🤓

/ 10/16/2025

Do you know the difference between home value vs. price in Metro Detroit? I will bust some myths and reveal…

Read More

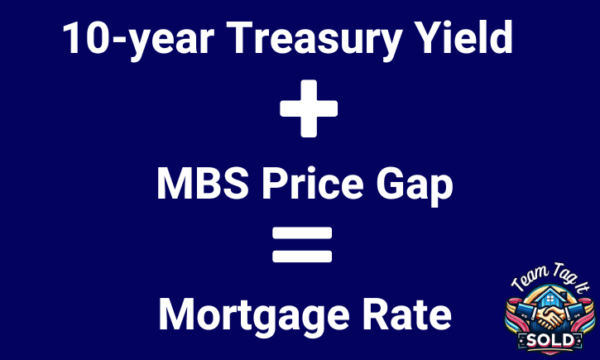

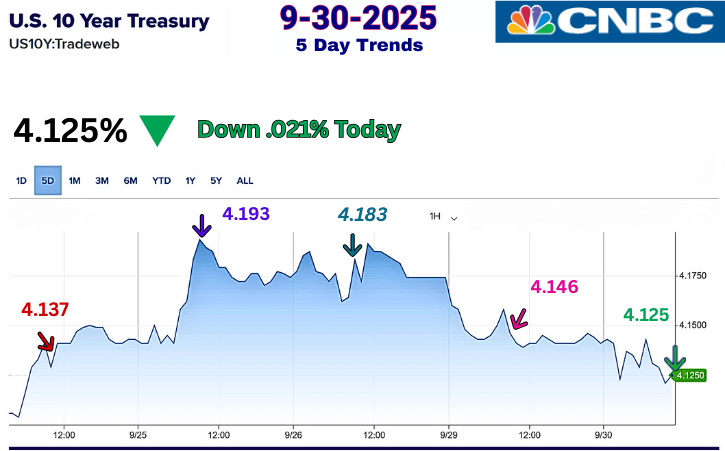

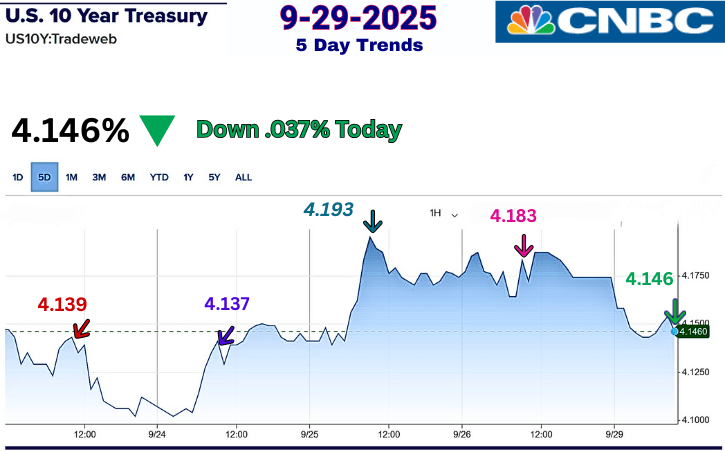

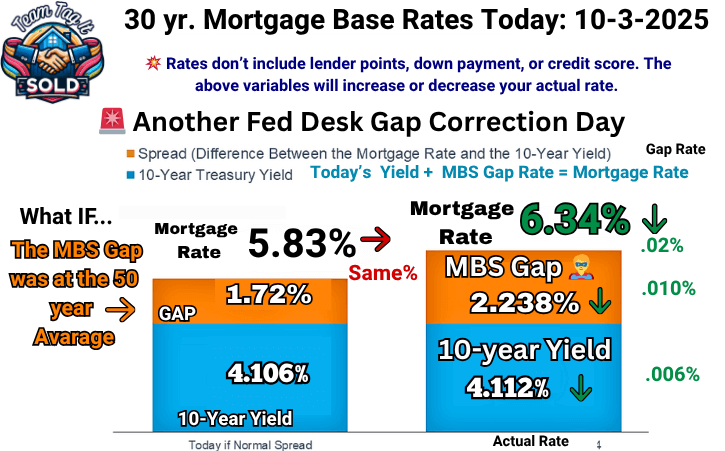

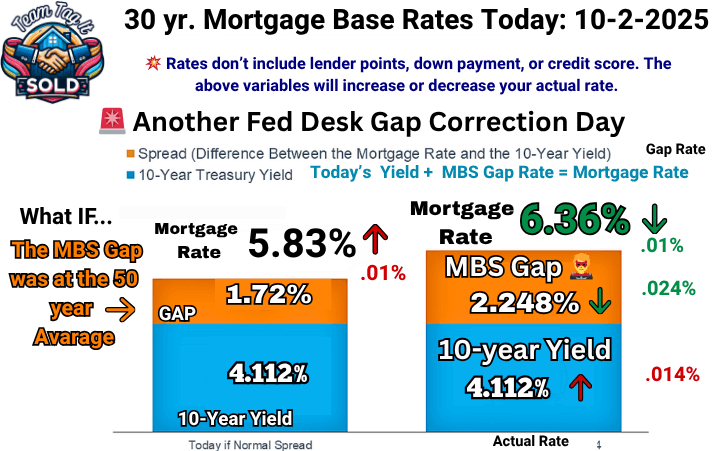

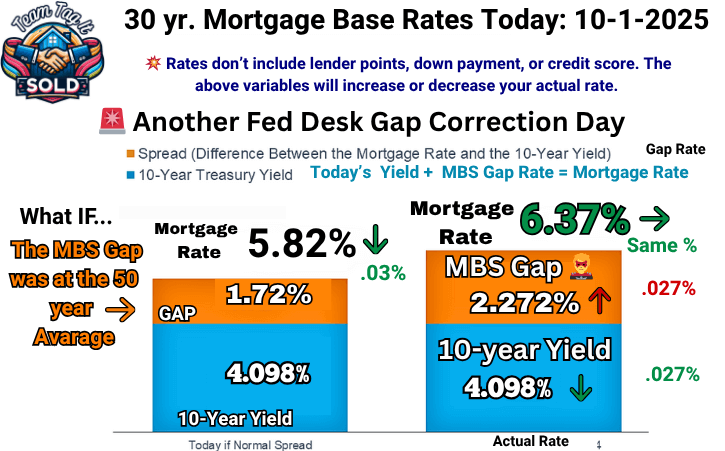

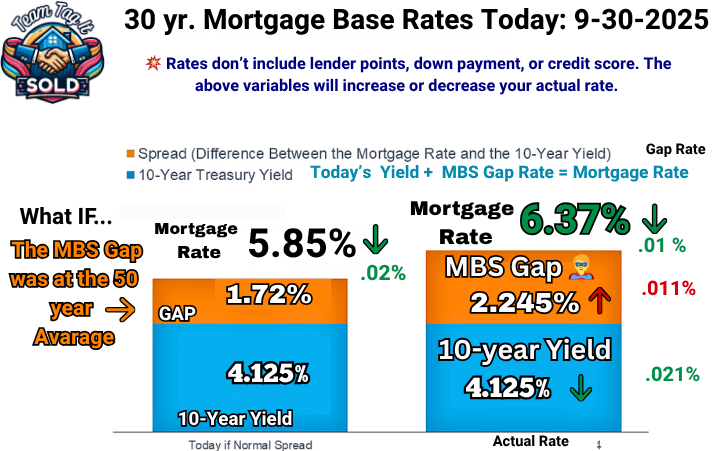

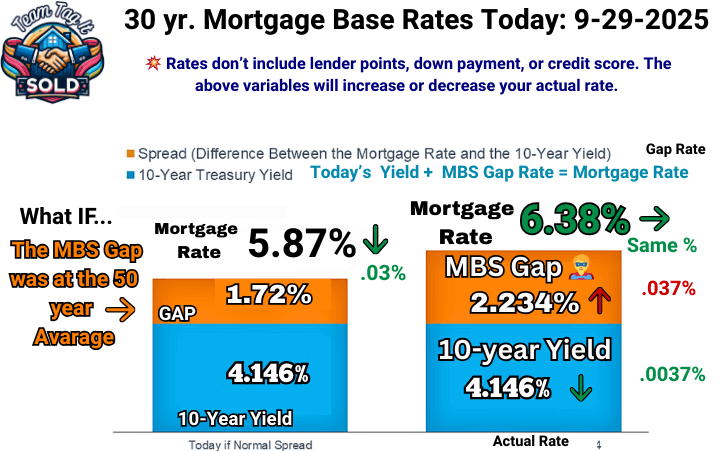

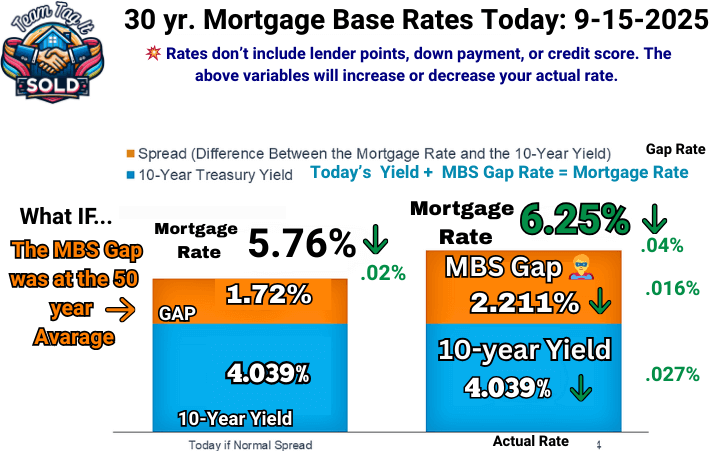

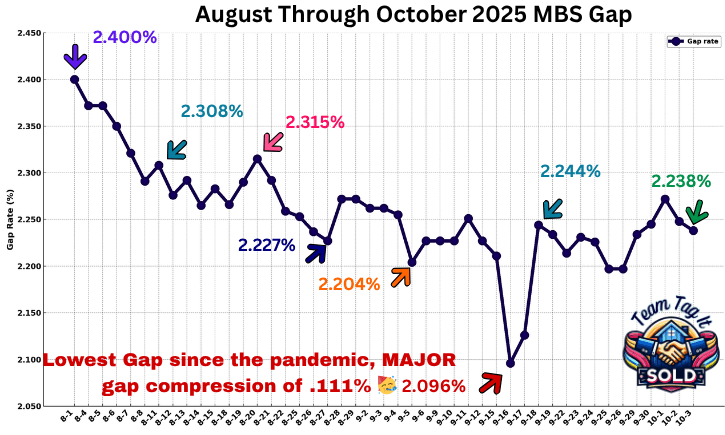

Mortgage-backed Securities Effects on Mortgage Rates💲📉

By Pam Sawyer 🤓

/ 10/16/2025

Mortgage Rates these days are on a roller coaster ride for Metro Detroit. To better predict where they are heading…

Read More

Negotiation Strategies for Home Buyers and Sellers 🙌🏡

By Pam Sawyer 🤓

/ 10/16/2025

Mastering negotiation strategies can make or break a deal for home buyers and sellers in Metro Detroit. Whether you’re trying…

Read More

Your Home Equity Gains: Game Changer When You Sell🏠📈

By Pam Sawyer 🤓

/ 10/16/2025

Discover how home equity can be a total game-changer when selling your home or exploring financial opportunities! 🚀 This article…

Read More

Mortgage Pre-Approval: The Secret Power Buyers Need to Know 🎓💲

By Pam Sawyer 🤓

/ 10/15/2025

Thinking🤔 about buying a home? 🏡 This blog post breaks down everything you need to know about mortgage pre-approval—the secret…

Read More

Buying a Fixer-Upper: Hidden Benefits Most Buyers Overlook 👀

By Pam Sawyer 🤓

/ 10/15/2025

Finding the perfect home in Metro Detroit can be challenging, especially with rising prices and limited options. But what if…

Read More

Is it Still a Sellers Market Today in Metro Detroit🏡❓

By Pam Sawyer 🤓

/ 10/14/2025

Is it still a Sellers Market in Metro Detroit today? I’ll show you how you can explore what is happening…

Read More

Will Foreclosures Crash the Housing Market in Metro Detroit Winter 2025

By Pam Sawyer 🤓

/ 10/13/2025

Do you ever tire of hearing about all those gloomy predictions for the future? Let’s review: Will Foreclosure Crash the…

Read More

Home Pricing Missteps: What Every Metro Detroit Seller Should Know

By Pam Sawyer 🤓

/ 10/12/2025

What every Metro Detroit Home Seller should know about Home Pricing Misteps. We’ll review the problems, and at the…

Read More

How to Choose the Right Buyers Agent: A Must for Home Buyers’ 🛒

By Pam Sawyer 🤓

/ 10/10/2025

In our blog post “What Should a Buyer’s Agent Really Do? ” We delve into the essential role of a…

Read More

Real Estate Guides for Buying & Selling ~ Metro Detroit Video🏡📰

By Pam Sawyer 🤓

/ 10/07/2025

Your Real Estate Guides will help you succeed in Home Buying and Home Selling in Metro Detroit. https://youtu.be/s335kYgtG9M 📢 Get…

Read More

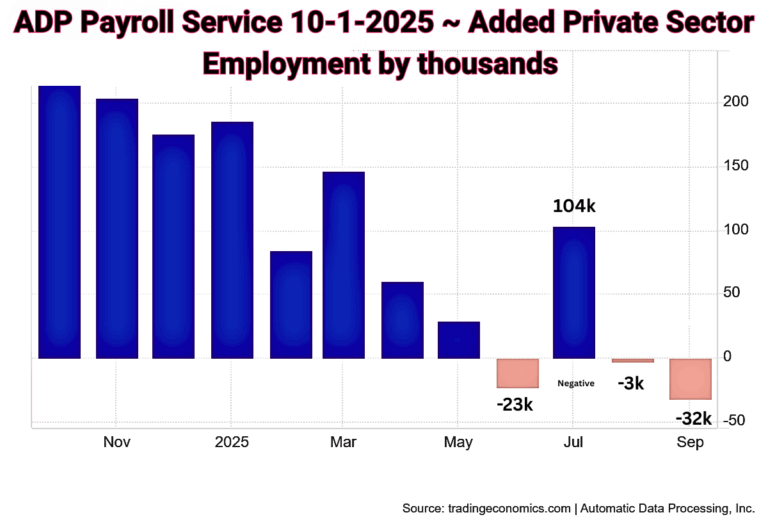

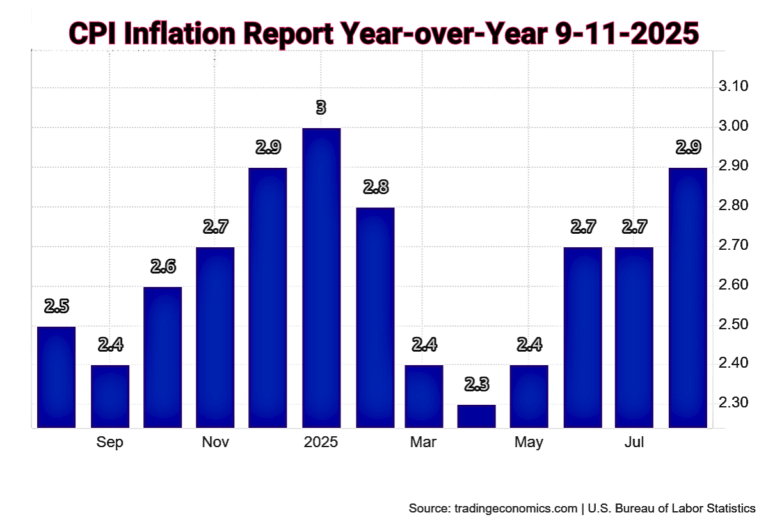

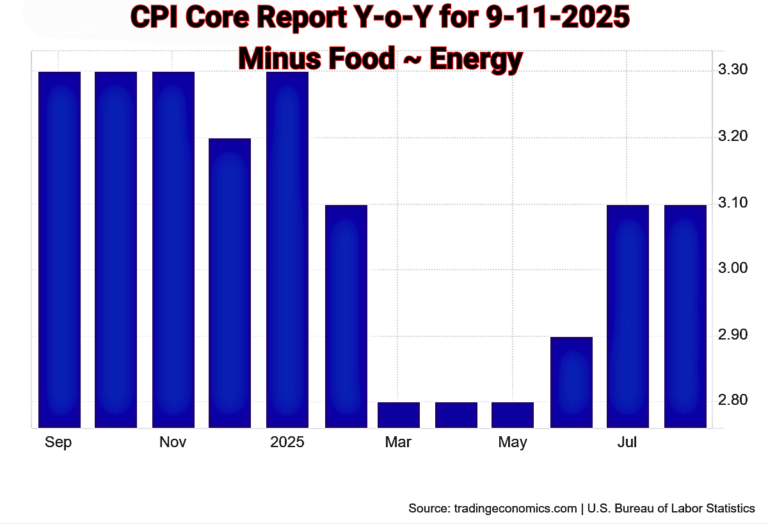

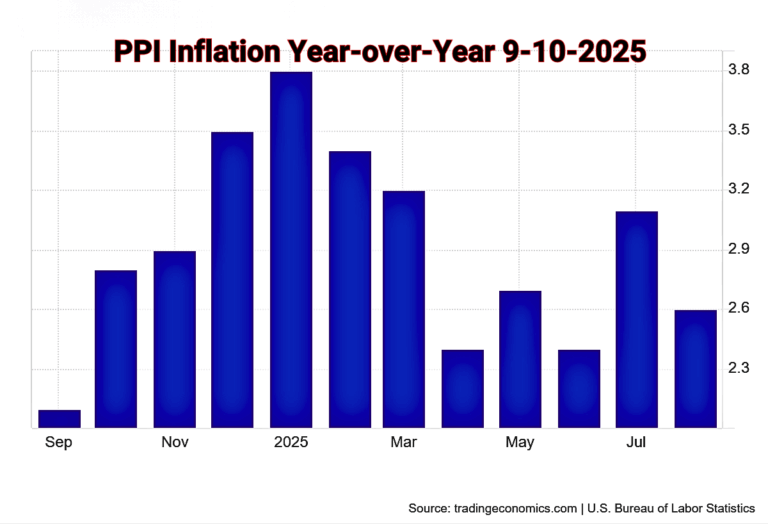

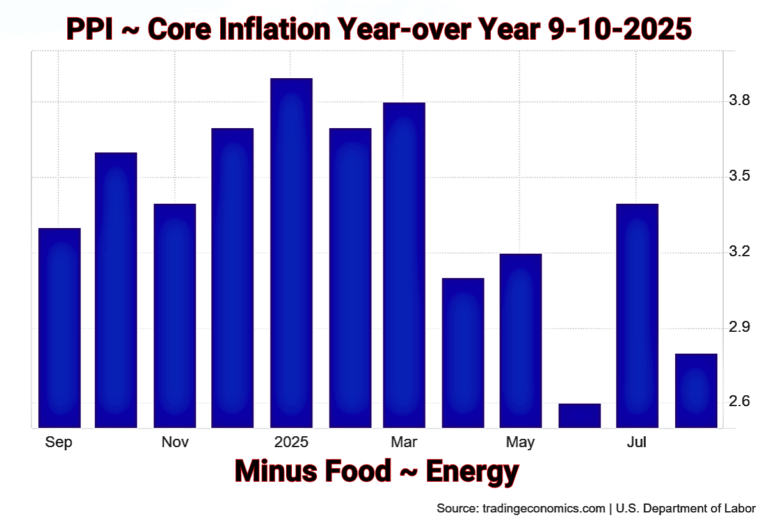

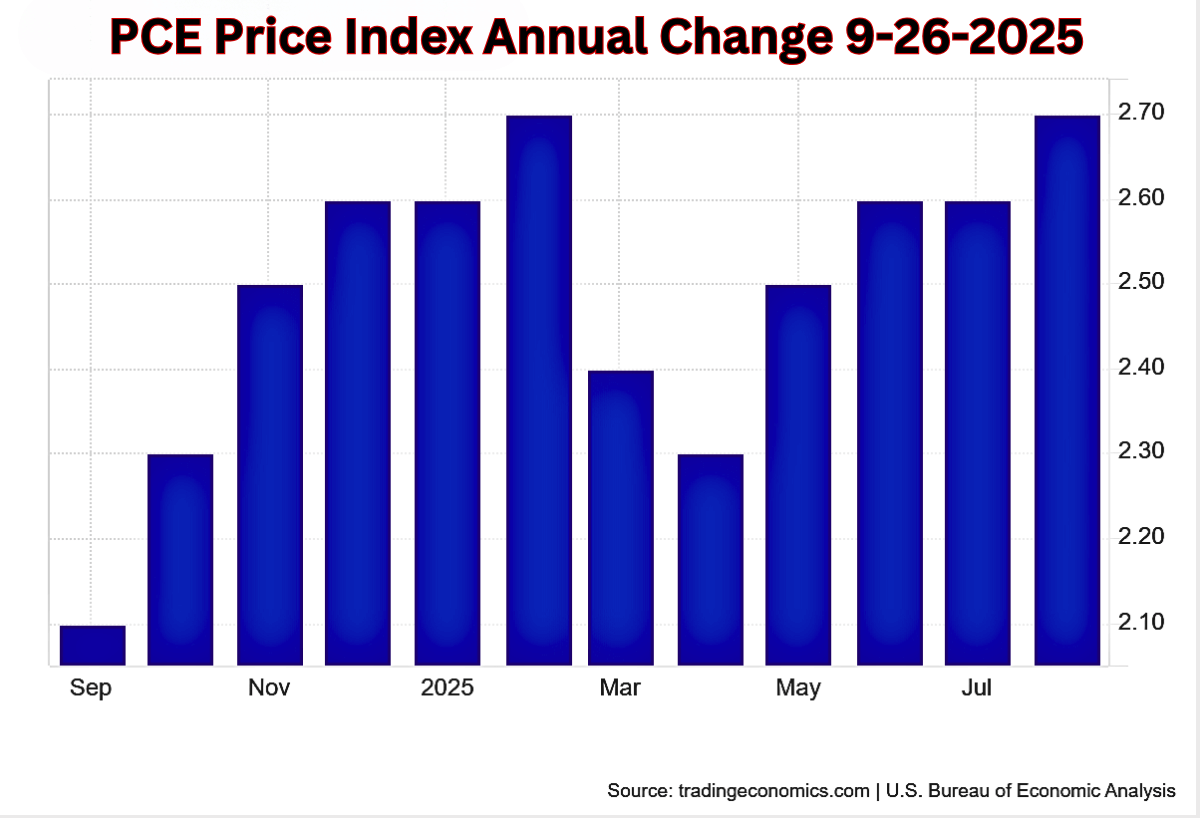

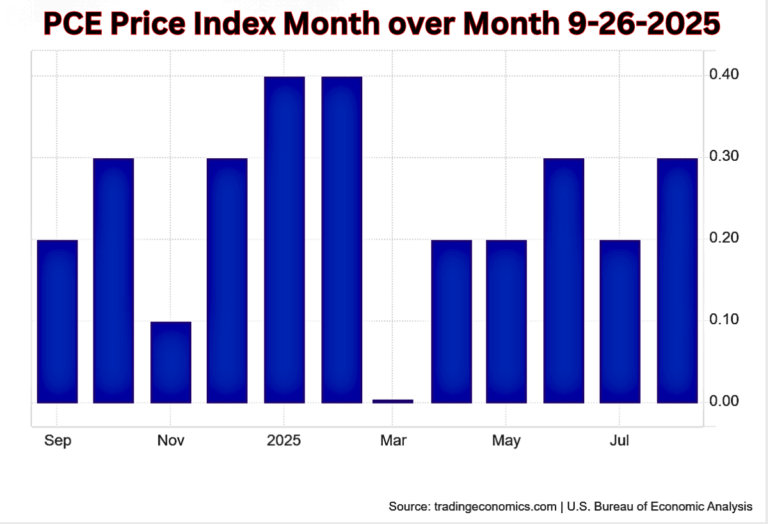

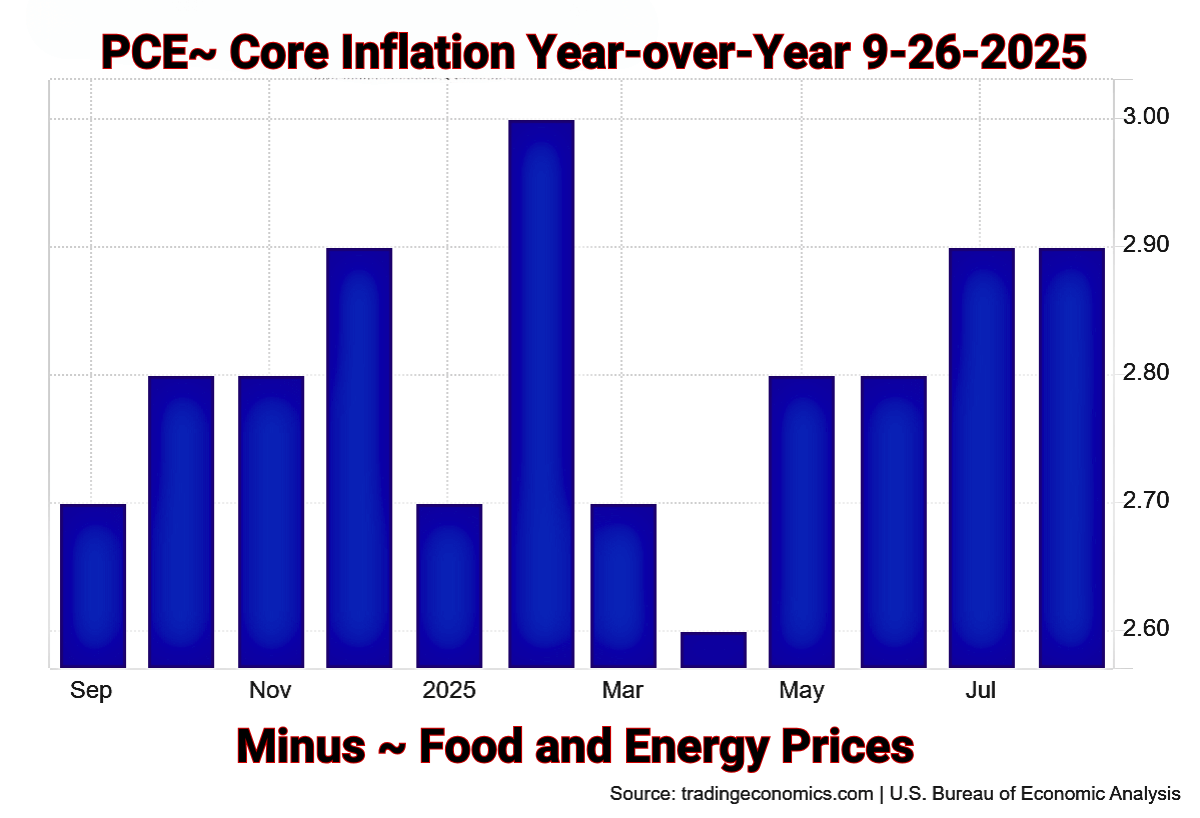

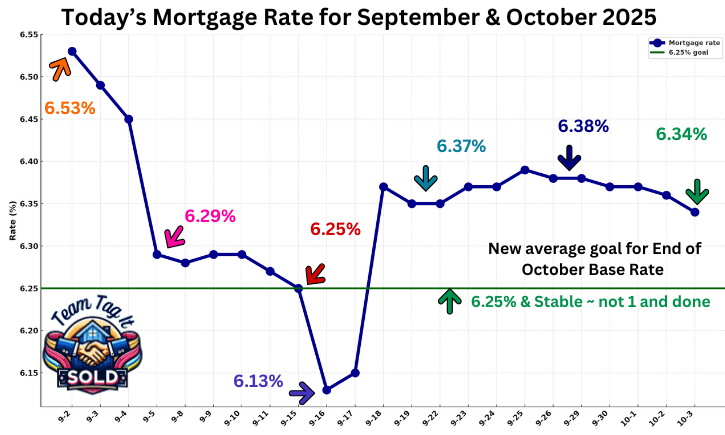

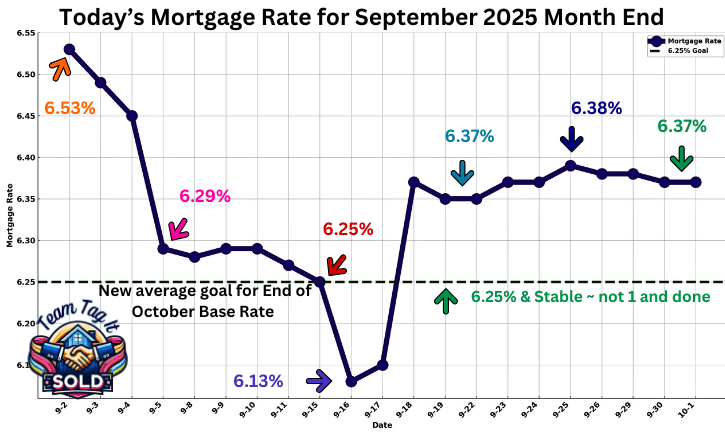

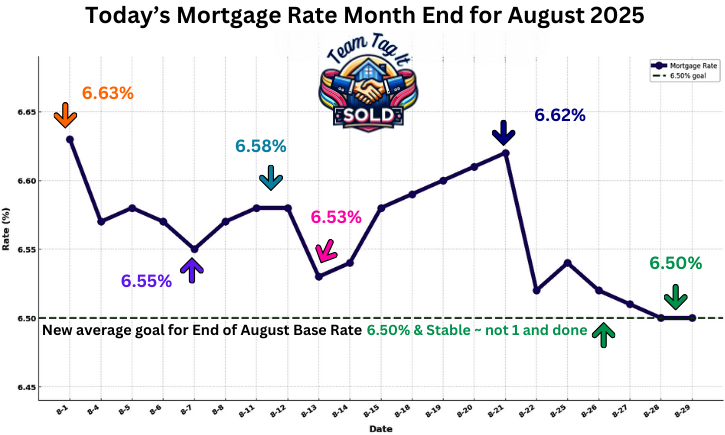

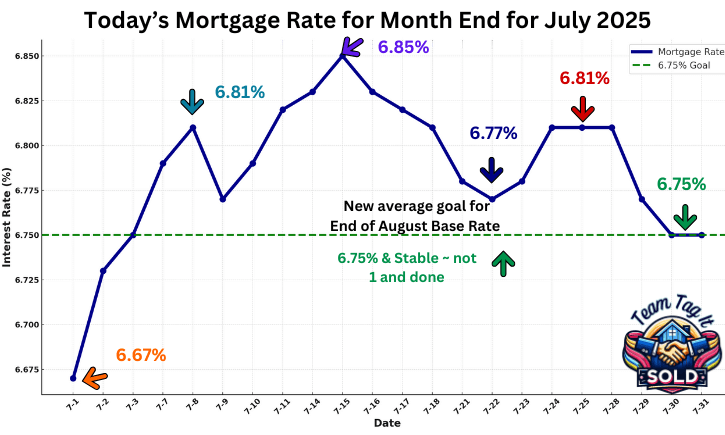

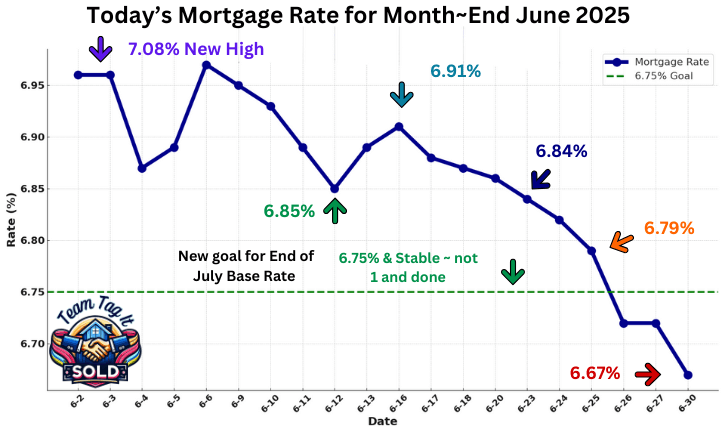

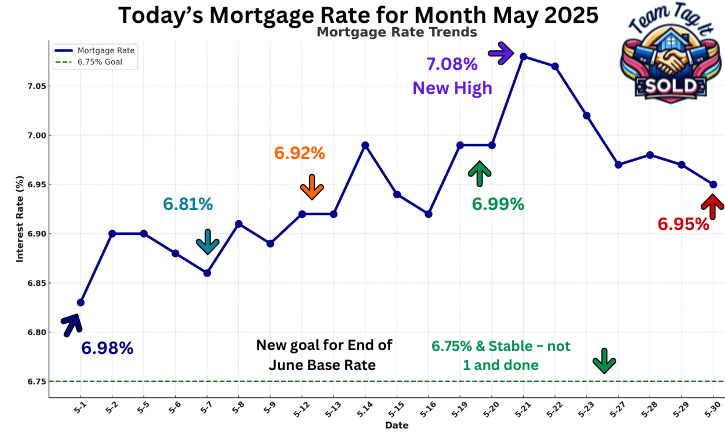

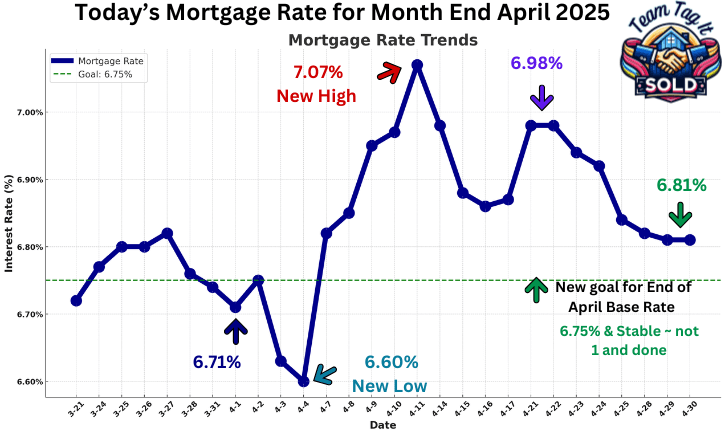

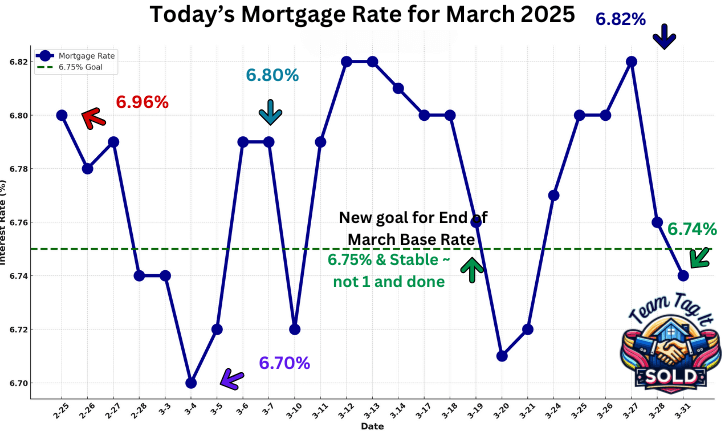

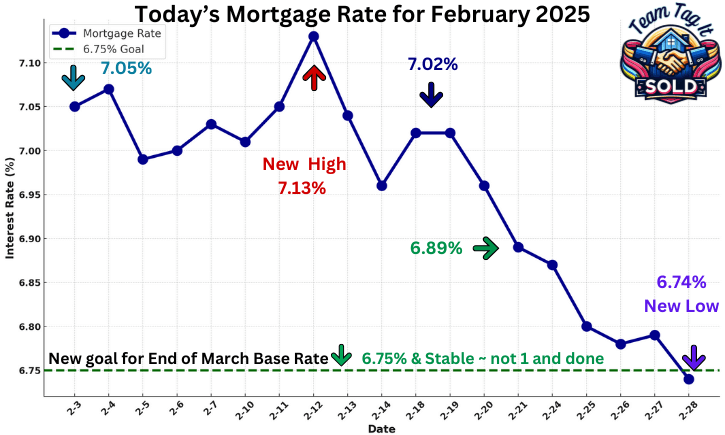

Crack the Mortgage Rate Code: Know the Why💡 and Save💲

By Pam Sawyer 🤓

/ 10/05/2025

To know where we’re going, we must review where we’ve been. Crack the Mortgage Rate Code reveals how to spot…

Read More

What Is A True Real Estate Expert: How to Find One🏡💥

By Pam Sawyer 🤓

/ 10/05/2025

We’ll explore the importance of finding a true real estate expert in Metro Detroit’s complex housing market. Why You Need…

Read More

Selling Your House As-Is OR Make Repairs Pros🌟 and Cons🚫

By Pam Sawyer 🤓

/ 10/03/2025

Selling a home can feel overwhelming, especially if it needs repairs. But what if you could skip the hassle and…

Read More

Top 3 Home Selling Questions in Metro Detroit Answered 🏡❓

By Pam Sawyer 🤓

/ 10/01/2025

Are you thinking about selling your home in Metro Detroit but unsure if now is the right time? 🤔🏡 This…

Read More

Top Real Estate Agent Skills for Selling Your Home🏡💲

By Pam Sawyer 🤓

/ 09/30/2025

Are you thinking of selling your home in Metro Detroit? Look for these top real estate agent skills to sell…

Read More

Thinking of Selling Your House: How Long Will It Take?

By Pam Sawyer 🤓

/ 09/29/2025

If you’re considering Selling Your House in Metro Detroit, you may be curious how long it should take. Let’s find…

Read More

Is Now a Good Time to Sell Your House❓Let’s Find Out 🥳

By Pam Sawyer 🤓

/ 09/26/2025

Wondering if now is a good time to sell your house in Metro Detroit? 🏡 This post explores market trends…

Read More

Downsizing Your Home Can Help You Fuel Your Retirement🤩🏡💲

By Pam Sawyer 🤓

/ 09/21/2025

When you retire, consider the opportunity to downsize your home in Metro Detroit and make your life easier. This blog…

Read More

Master Your Mortgage Rate: Control the Controllable💰🏡

By Pam Sawyer 🤓

/ 09/20/2025

Knowing today’s mortgage rate is one thing. You need to learn how to Master Your Mortgage Rate and save money…

Read More

Inspection vs. Appraisal: Understaning the Key Difference🕵️🏡💲

By Pam Sawyer 🤓

/ 09/18/2025

When buying a home in Metro Detroit, understanding the difference between a home inspection and an appraisal is key! A…

Read More

Discover How Home Equity Can Fund Your Next Move💰

By Pam Sawyer 🤓

/ 09/18/2025

Discover how home equity can be a total game-changer when selling your home or exploring financial opportunities! 🚀 This article breaks down what home equity is, why…

Read More

Metro Detroit Sold Home Prices by City: Live MLS Data🥳🏘️

By Pam Sawyer 🤓

/ 09/11/2025

Metro Detroit Sold Home Prices gives you a clear view of what homes are really selling for, updated daily with…

Read More

Should You Rent or Sell Your House❓🏡

By Pam Sawyer 🤓

/ 09/04/2025

📢 Should You Rent or Sell Your House in Metro Detroit? 🏡💰 This guide breaks down the pros and cons…

Read More

How to Market Your House for More Money💲🏡🎥

By Pam Sawyer 🤓

/ 09/01/2025

Want to sell your house for more money in Metro Detroit? 🏡 This guide shows you how to use smart…

Read More

How to Tell if Your House is Priced Right? Let’s Find Out 💲🤯

By Pam Sawyer 🤓

/ 07/16/2025

🏡 Thinking about selling your home or already have it on the market? 🤔 Wondering if your house is priced right? 👉…

Read More

More Help Is 1️⃣ Click Away⤵️

Adjustable Rate Mortgage (ARM): Smart Move or Mistake❓

By Pam Sawyer 🤓

/ 10/25/2025

Thinking about an 🔁 Adjustable Rate Mortgage (ARM) in today’s market? Discover how ARMs work, what’s changed since the 2008 crash,…

Read More

Today’s Mortgage Rate: Your Why Alert with Video 📢

By Pam Sawyer 🤓

/ 10/24/2025

Today’s Mortgage Rates: Let’s crack the code 🔢 for Metro Detroit and take control of your home financing! The video will help…

Read More

Metro Detroit Home Prices and Real Estate Trends by City~Oct.📊

By Pam Sawyer 🤓

/ 10/23/2025

🎯 Want the latest scoop on Metro Detroit home prices? 📊🏡 Our live MLS data and interactive charts keep you…

Read More

Home Value vs Price in Metro Detroit: Myth Busting Revealed 🤫

By Pam Sawyer 🤓

/ 10/16/2025

Do you know the difference between home value vs. price in Metro Detroit? I will bust some myths and reveal…

Read More

Mortgage-backed Securities Effects on Mortgage Rates💲📉

By Pam Sawyer 🤓

/ 10/16/2025

Mortgage Rates these days are on a roller coaster ride for Metro Detroit. To better predict where they are heading…

Read More

Negotiation Strategies for Home Buyers and Sellers 🙌🏡

By Pam Sawyer 🤓

/ 10/16/2025

Mastering negotiation strategies can make or break a deal for home buyers and sellers in Metro Detroit. Whether you’re trying…

Read More

Your Home Equity Gains: Game Changer When You Sell🏠📈

By Pam Sawyer 🤓

/ 10/16/2025

Discover how home equity can be a total game-changer when selling your home or exploring financial opportunities! 🚀 This article…

Read More

Mortgage Pre-Approval: The Secret Power Buyers Need to Know 🎓💲

By Pam Sawyer 🤓

/ 10/15/2025

Thinking🤔 about buying a home? 🏡 This blog post breaks down everything you need to know about mortgage pre-approval—the secret…

Read More

Buying a Fixer-Upper: Hidden Benefits Most Buyers Overlook 👀

By Pam Sawyer 🤓

/ 10/15/2025

Finding the perfect home in Metro Detroit can be challenging, especially with rising prices and limited options. But what if…

Read More

Is it Still a Sellers Market Today in Metro Detroit🏡❓

By Pam Sawyer 🤓

/ 10/14/2025

Is it still a Sellers Market in Metro Detroit today? I’ll show you how you can explore what is happening…

Read More

Will Foreclosures Crash the Housing Market in Metro Detroit Winter 2025

By Pam Sawyer 🤓

/ 10/13/2025

Do you ever tire of hearing about all those gloomy predictions for the future? Let’s review: Will Foreclosure Crash the…

Read More

Home Pricing Missteps: What Every Metro Detroit Seller Should Know

By Pam Sawyer 🤓

/ 10/12/2025

What every Metro Detroit Home Seller should know about Home Pricing Misteps. We’ll review the problems, and at the…

Read More

How to Choose the Right Buyers Agent: A Must for Home Buyers’ 🛒

By Pam Sawyer 🤓

/ 10/10/2025

In our blog post “What Should a Buyer’s Agent Really Do? ” We delve into the essential role of a…

Read More

Real Estate Guides for Buying & Selling ~ Metro Detroit Video🏡📰

By Pam Sawyer 🤓

/ 10/07/2025

Your Real Estate Guides will help you succeed in Home Buying and Home Selling in Metro Detroit. https://youtu.be/s335kYgtG9M 📢 Get…

Read More

Crack the Mortgage Rate Code: Know the Why💡 and Save💲

By Pam Sawyer 🤓

/ 10/05/2025

To know where we’re going, we must review where we’ve been. Crack the Mortgage Rate Code reveals how to spot…

Read More

What Is A True Real Estate Expert: How to Find One🏡💥

By Pam Sawyer 🤓

/ 10/05/2025

We’ll explore the importance of finding a true real estate expert in Metro Detroit’s complex housing market. Why You Need…

Read More

Selling Your House As-Is OR Make Repairs Pros🌟 and Cons🚫

By Pam Sawyer 🤓

/ 10/03/2025

Selling a home can feel overwhelming, especially if it needs repairs. But what if you could skip the hassle and…

Read More

Top 3 Home Selling Questions in Metro Detroit Answered 🏡❓

By Pam Sawyer 🤓

/ 10/01/2025

Are you thinking about selling your home in Metro Detroit but unsure if now is the right time? 🤔🏡 This…

Read More

Top Real Estate Agent Skills for Selling Your Home🏡💲

By Pam Sawyer 🤓

/ 09/30/2025

Are you thinking of selling your home in Metro Detroit? Look for these top real estate agent skills to sell…

Read More

Thinking of Selling Your House: How Long Will It Take?

By Pam Sawyer 🤓

/ 09/29/2025

If you’re considering Selling Your House in Metro Detroit, you may be curious how long it should take. Let’s find…

Read More

Summary

Article Name

Crack the Mortgage Rate Code: Know the Why 💡and Save💲

DescriptionUnlock the secrets and Crack the Mortgage Rate Code for Metro Detroit. Learn how to predict where mortgage rates are heading🤩 Empower your move and know when mortgage rates will drop🥳🎉

Author

Pam Sawyer, Realtor🤓

Publisher Name

Metro Detroi Home Experts | Team Tag It Sold

Publisher Logo