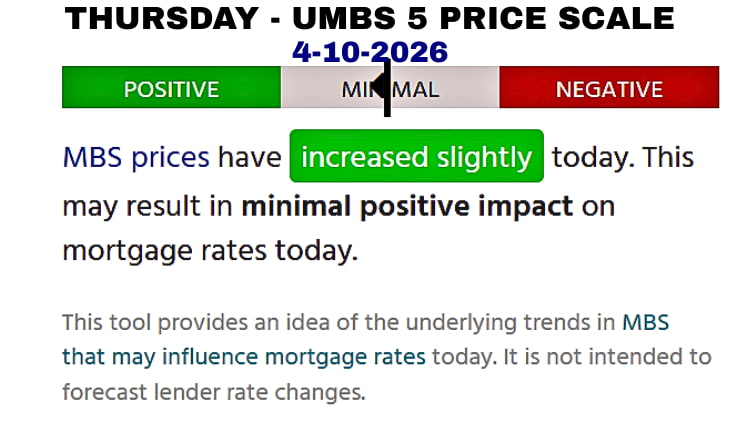

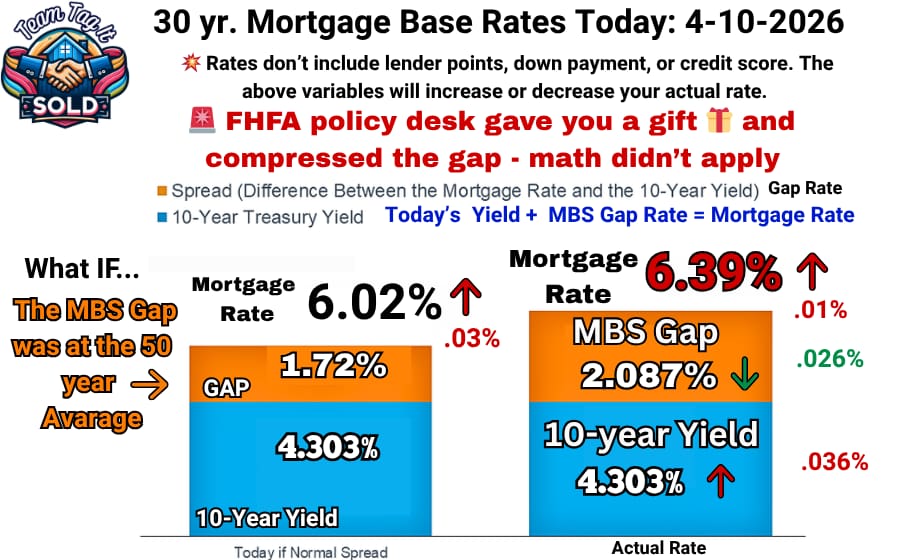

Risk Premium Colapse- Yield Plummetted 4-10-2026 📉 – Updates coming at 10:00 & 10:30 AM and 12-1:00 Anchor

I’m on market watch again 👀. The US bond market is suddenly flashing a warning sign about the economy before the conflict in Iran. We now have a yield pattern. Wall Street is reacting to the headlines. If they read “hope” and “less risk,” the yield drifts down.📉 If the headlines read “escalation” and “increased risk,” then we see the spike.📈 Today, the yield is reacting to the headlines and the details of the WHY below. ⤵️By 10:00, the yield had drifted higher to 4.311% and remains steady. I will use the 10:30 yield rate to gauge where mortgage rates could land Today. See details below in step 2. ⤵️Yesterday, same numbers and different day. The FHFA policy desk kept rates unchanged, then repriced them lower. Today we start lower and could reprice higher.

Step 1: WHY the Yield Plummetted, and Mortgage Rates will follow📉

Mortgage rates moved higher in the afternoon yesterday as bond yields drifted higher, and mortgage rates followed with an afternoon revision. ⚠️ Today, it is a carryover of a very unstable bond and securities market. The bond market is pricing the possibility of stability, not proof of it. The underlying risks associated with global shipping, energy flows, and geopolitical control remain unresolved. That means volatility isn’t behind us—it’s just entering a new phase, and the Yo-Yo effect will continue as Wall Street tries to price in risk. Inflation CPI reports are on the back burner and didn’t affect the bond market this morning. Wall Street is back to watching the headlines.

What the Bond Market Is Actually Watching🔍

🚢 “Strait of Hormuz Open” Doesn’t Mean Risk Is Gone

- A ceasefire announcement is not the same as operational flow

- Oil only moves when logistics are active—not when headlines hit

- Tankers, crews, and contracts must all align before supply resumes

- Market reaction = relief, not confidence

📝 Insurance Is the Real Gatekeeper

- Coverage depends on enforceability and security—not politics

- Key questions still unanswered:

- Who guarantees safe passage?

- Are escorts active?

- Is compliance being monitored?

- Without coverage, shipping stays frozen—or becomes too expensive to operate

⭐ The 14-Day Window Is the Pressure Point

- Tanker cycle timing leaves almost no margin for delays

- Any disruption—weather, inspections, or conflict—resets the clock

- Markets are trading this window as a live risk event

📊 Expect Volatility, Not a Smooth Trend

- Today’s yield drop = short-term relief move

- Next moves will depend on real-world confirmations:

- Tanker activity

- Insurance approvals

- Military presence

- Political follow-through

- One headline down → next headline up. That’s the environment

🧭 Final Takeaway

The ceasefire bought time—but didn’t fix the system.

The bond market is reacting to hope, not proof.

Until oil physically flows and risk is priced out, mortgage rates will remain unstable.